Study · Kresmion Research

Inside Amazon: Where the Money Comes From, Why the Cloud Earns the Profit, and Why It Builds Its Own Chips

Amazon looks like a retailer, but most of its profit comes from Amazon Web Services, a fast growing advertising business, and chips it designs in house. This study walks through where the money actually comes from, how the company got here, what it is spending on next, and the risks attached, without telling you what to do about any of it.

The headline fact about Amazon in 2026 is the gap between revenue and profit: retail generates most of the $716.9 billion in sales, but Amazon Web Services produced about 57 percent of operating income on roughly 18 percent of revenue, and a roughly $200 billion capital program is now reshaping the whole company around artificial intelligence.

Key takeaways

| Measure | Reading | Source |

|---|---|---|

| FY2025 revenue | $716.9 billion, up 12.4 percent | Amazon FY2025 10-K |

| FY2025 operating income | $80.0 billion, margin 11.2 percent | Amazon FY2025 10-K |

| AWS FY2025 | $128.7 billion revenue, $45.6 billion operating income, 35.4 percent margin | Amazon FY2025 10-K |

| AWS share of profit | About 57 percent of operating income on about 18 percent of revenue | Amazon FY2025 10-K |

| Advertising FY2025 | $68.6 billion, up about 22 percent | Amazon FY2025 10-K |

| Custom chips | Graviton CPUs are more than half of new AWS CPU capacity; Trainium powers AI training | AWS, re:Invent 2025 |

| 2026 capital plan | About $200 billion, predominantly AWS and AI | Amazon, Q4 2025 release |

| Free cash flow | Fell from $38.2 billion to $11.2 billion as capex surged | Amazon, Q4 2025 release |

From bookstore to four businesses in one

Amazon started as an online bookseller in 1994 and spent its first two decades widening into an "everything store" and a logistics network. What matters for understanding the company today is that it is no longer one business. It reports three operating segments, and inside them sit several very different economic engines.

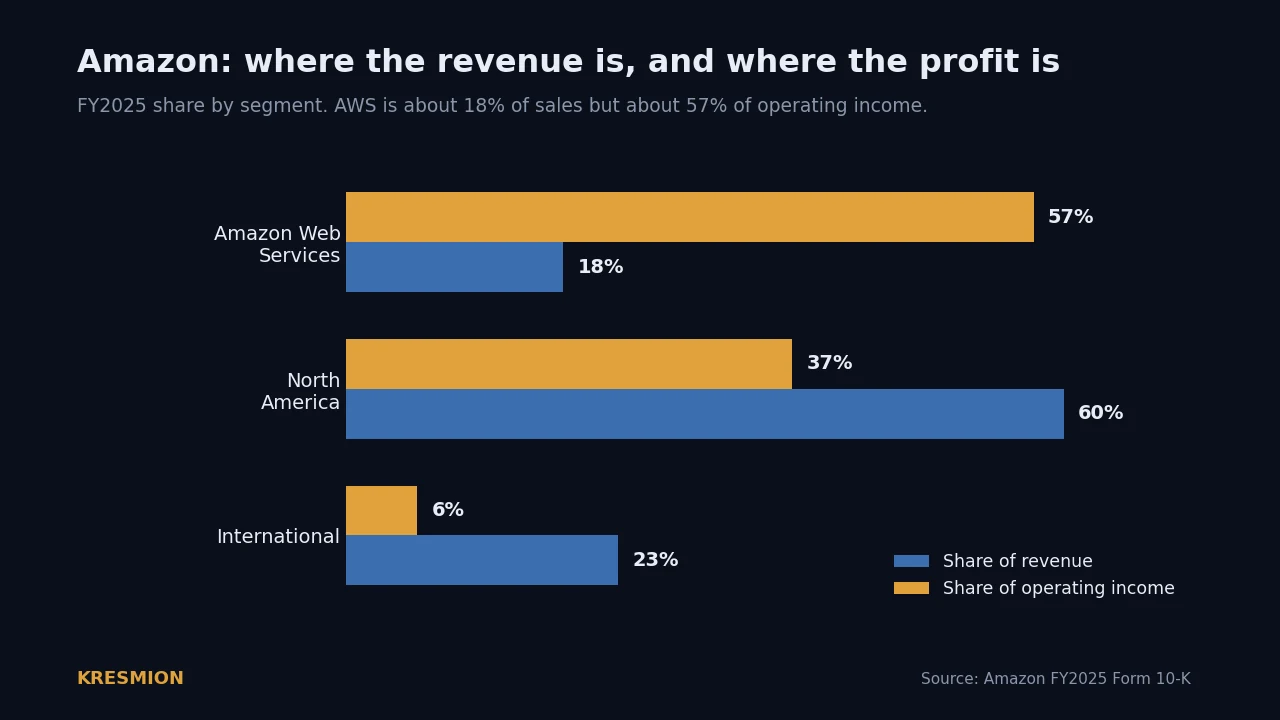

For the 2025 fiscal year, which Amazon runs on the calendar, the three segments were North America at $426.3 billion in sales with $29.6 billion of operating income, International at $161.9 billion with $4.7 billion of operating income, and Amazon Web Services at $128.7 billion with $45.6 billion of operating income (Amazon FY2025 10-K). The pattern is the whole story in one line: the two retail segments are about 82 percent of revenue but thin on margin, while AWS is about 18 percent of revenue and produced roughly 57 percent of the company's $80.0 billion in operating income.

Amazon also discloses revenue by type of product or service, which shows where growth is concentrated. In FY2025, online stores were $269.3 billion (up 9.0 percent), third party seller services $172.2 billion (up 10.3 percent), AWS $128.7 billion (up 19.7 percent), advertising services $68.6 billion (up 22.1 percent), subscription services $49.6 billion (up 11.8 percent), and physical stores $22.6 billion (up 6.3 percent) (Amazon FY2025 10-K). The fastest growing large line is advertising, and the most profitable is the cloud. The first party retail business, the part most people picture when they think of Amazon, is the slowest grower of the major lines.

The past five years: a loss, then a sharp recovery

Amazon's recent history is not a smooth climb. Revenue rose from about $469.8 billion in 2021 to $716.9 billion in 2025, but profitability swung hard along the way. In 2022 the company posted a net loss of about $2.7 billion, driven mainly by a roughly $12.7 billion writedown on its stake in the electric vehicle maker Rivian, plus over built warehouse capacity and cost inflation (Seattle Times). Operating income that year fell to roughly $12.2 billion.

Then came one of the larger corporate turnarounds of the decade. Under chief executive Andy Jassy, Amazon cut costs, regionalized its US logistics network to shorten delivery distances, and let cloud and advertising compound. Operating income climbed from about $12.2 billion in 2022 to $36.9 billion in 2023, $68.6 billion in 2024, and $80.0 billion in 2025 (Amazon FY2025 10-K). Net income reached $77.7 billion in 2025, with diluted earnings of $7.17 per share, and operating cash flow rose about 20 percent to $139.5 billion (Amazon Q4 2025 release). The International segment, a chronic money loser, turned solidly profitable.

AWS: the profit engine, re-accelerating

Amazon Web Services is the cloud computing arm that rents servers, storage, databases, and increasingly artificial intelligence to other companies. It is the single most important driver of Amazon's profitability. In FY2025 AWS earned $45.6 billion of operating income at a 35.4 percent margin (Amazon FY2025 10-K).

After a slower stretch in 2023, when customers were cutting cloud bills, AWS growth has re-accelerated for several quarters in a row. In the first quarter of 2026, the three months ended March 31, AWS revenue reached $37.6 billion, up 28 percent year over year, which Amazon described as its fastest growth in roughly 15 quarters, at an operating margin near 37.7 percent and an annualized run rate around $150 billion (Amazon Q1 2026 release, CNBC). Management has repeatedly said the AI business is capacity constrained, meaning it could sell more if it could build data centers and install chips faster.

Two cautions belong next to that growth. First, AWS is still slowly ceding relative market share. Synergy Research put first quarter 2026 cloud infrastructure share at about 28 percent for AWS, 21 percent for Microsoft Azure, and 14 percent for Google Cloud, with AWS down from a little over 32 percent in 2021 as rivals grew faster (Synergy Research). Second, the demand is real and contracted: AWS reported a backlog of customer commitments of about $364 billion as of March 31, 2026, with a weighted average life of 5.5 years, and that figure excludes a separate commitment of more than $100 billion tied to the AI developer Anthropic (Amazon Q1 2026 10-Q).

The chip strategy: why Amazon designs its own silicon

One of the most distinctive things about Amazon, and the part that surprises people, is that it is now a serious chip designer. This did not happen overnight. In 2015 Amazon bought a small Israeli chip design firm, Annapurna Labs, in a deal reported at around $350 million that was never officially confirmed (GeekWire). That team now designs four families of custom chips, and the strategic logic is consistent across all of them: owning the silicon lets AWS lower the cost of each unit of computing, improve margins, and depend less on outside suppliers.

The first product was the Nitro System, a set of dedicated cards and a lightweight hypervisor that offload networking, storage, and security tasks from the main processor so that nearly all of a server's power goes to the customer. Nitro now sits in every AWS server (Amazon Science).

Next came Graviton, Amazon's line of general purpose processors built on Arm designs rather than the x86 chips sold by Intel and AMD. The generations run from Graviton1 in 2018 to Graviton4 in 2024 and Graviton5, which reached general availability in June 2026 on a 3 nanometer process with 192 cores (AWS). Amazon markets Graviton at up to 40 percent better price for performance and up to 60 percent less energy than comparable x86 instances, and at its December 2025 conference it said that for the third year running, more than half of all new processor capacity it added was Graviton (AWS EC2 Graviton). In his 2025 shareholder letter, Jassy said two large customers each asked to buy Amazon's entire planned 2026 Graviton supply (Amazon shareholder letter).

For artificial intelligence, Amazon designs two more families. Inferentia chips handle inference, the running of trained models, and Trainium chips handle training, the building of them. Trainium2 became broadly available in December 2024 with claims of 30 to 40 percent better price for performance than comparable Nvidia GPU instances, and Trainium3, announced in December 2025, is Amazon's first 3 nanometer AI chip, claimed to deliver up to 4.4 times the compute of its predecessor (AWS Trainium2, AWS Trainium3).

The flagship proof point is Project Rainier, a giant cluster Amazon built for Anthropic, the maker of the Claude models. It launched with close to 500,000 Trainium2 chips, with a plan to exceed one million, giving Anthropic more than five times the computing power it used for its prior models (Amazon). Amazon has invested about $8 billion in Anthropic through 2024 and committed a further $5 billion in 2026, and Anthropic in turn has committed to spend more than $100 billion on AWS and to use up to 5 gigawatts of Amazon's own chips (Amazon).

It is important to be precise about the limits. Custom silicon does not mean Amazon has displaced Nvidia. Nvidia still dominates frontier model training, its CUDA software is a deep moat, and AWS continues to sell the newest Nvidia systems alongside its own chips. Amazon frames the two as complementary, and its next training chip is designed to work with Nvidia's networking. The honest reading is that custom chips give AWS a cost lever and supply insurance, not a clean break from Nvidia.

Advertising and the AI products most people will touch

Advertising is the quiet profit story. Amazon sells sponsored placements across its store and, since 2024, ads inside Prime Video, and that business reached $68.6 billion in FY2025, growing about 22 percent (Amazon FY2025 10-K). It is the third largest digital advertising business in the world behind Google and Meta, and because the incremental cost of showing an ad is low, its growth is unusually accretive to profit.

On the consumer side, Amazon has rebuilt its assistant and shopping tools around generative AI. It introduced its own Nova family of foundation models in late 2024 and a more capable Nova 2 generation in December 2025, all served through its Bedrock model platform and running heavily on Trainium (Amazon). It relaunched its voice assistant as Alexa+, a conversational and agentic version priced at $19.99 a month but free to Prime members, which passed one million users by June 2025 (Amazon). And its shopping assistant Rufus was used by about 250 million shoppers in 2025, which Amazon expects to drive more than $10 billion in annualized incremental sales (Fortune).

The other bets: satellites, robotaxis, robots, and a grocery retreat

Amazon runs a portfolio of longer dated projects. Project Kuiper, its low earth orbit satellite internet network, was renamed Amazon Leo in late 2025. It is authorized for about 3,236 satellites and had more than 350 in orbit by the middle of 2026, well behind its original schedule, which led the Federal Communications Commission to grant a conditional waiver on its deployment deadlines (SpaceNews, GeekWire). It is a distant challenger to SpaceX's Starlink, which has more than 10,000 satellites in service.

The robotaxi unit Zoox began offering public rides in Las Vegas in 2025, trailing Alphabet's Waymo (TechCrunch). In healthcare, Amazon owns the primary care provider One Medical, bought for $3.9 billion in 2023, and runs Amazon Pharmacy. And in warehouse robotics, Amazon said it had deployed more than one million robots by mid 2025, a fleet now approaching the size of its human workforce of about 1.56 million, coordinated by a generative AI model it calls DeepFleet (Amazon).

Not every bet expands. In January 2026 Amazon said it would close its own branded Amazon Go and Amazon Fresh physical stores and concentrate its grocery presence in Whole Foods, which it bought in 2017, plus online delivery (Amazon). The cashierless "Just Walk Out" technology that once defined Amazon Go is now positioned mainly as a product Amazon licenses to other venues.

The 2026 tension: a $200 billion bet

The defining financial fact of Amazon right now is the size of its spending. Capital expenditure rose from about $83 billion in 2024 to $131.8 billion in 2025, and Jassy guided to about $200 billion for 2026, predominantly for AWS because, in his words, the company has very high demand (Amazon Q4 2025 release). That is one of the largest capital programs in corporate history.

The cost shows up immediately in free cash flow, which Amazon's own release reported fell from $38.2 billion to $11.2 billion over the trailing year, a roughly 71 percent decline driven almost entirely by the increase in property and equipment purchases, not by any weakness in operations (Amazon Q4 2025 release). Depreciation is rising too, from $52.8 billion to $65.8 billion, and Amazon shortened the assumed useful life of its servers from six years back to five in 2025, citing faster obsolescence in the AI era, which pulls more cost into the near term.

This is where reasonable observers disagree, and the debate is worth stating from both sides. Amazon's position, in Jassy's words, is that it is not spending on a hunch but against contracted customer demand, and that it is willing to accept short term cash flow headwinds for a larger long term payoff (CNBC). The skeptical position, voiced by analysts and ratings agencies, is that the entire hyperscale industry may be overbuilding AI capacity, with combined spending heading toward roughly $700 billion in 2026, and that the returns on it are not yet proven (DataCenterDynamics). Both statements are true at the same time, and which one matters more will be visible only in later results.

Risks and regulation

Amazon faces an unusually broad set of legal and regulatory pressures. The Federal Trade Commission sued the company in September 2023, alleging it illegally maintains monopoly power in online retail through anti discounting tactics and pressure on sellers to use its fulfillment network. A judge let most of the case proceed in 2024, and the trial has been scheduled for March 2027 (FTC, MLex). Separately, in September 2025 Amazon agreed to a $2.5 billion settlement with the FTC, a $1 billion civil penalty plus $1.5 billion in consumer refunds, over deceptive Prime sign up and cancellation practices (FTC). In Europe, Amazon's marketplace is a designated gatekeeper under the Digital Markets Act, and in November 2025 a European court upheld its obligations as a very large platform under the Digital Services Act.

Beyond regulation, the competitive map is crowded on every front: Microsoft Azure and Google Cloud are growing faster in the cloud, Walmart and the low cost importers Temu and Shein press on retail, Google and Meta still dwarf Amazon in advertising, and Microsoft, OpenAI, and Google compete directly in AI. Amazon is also exposed to the health of consumer spending, to tariff and trade policy that affects its many China based third party sellers, and to labor questions, including unionization efforts and the social friction of automating warehouse jobs. In October 2025 it announced about 14,000 corporate layoffs, citing its AI investment.

How to read the valuation, without a recommendation

For context only, and not as advice, here is how the market priced Amazon in mid June 2026. The stock closed at $244.39 on June 18, giving a market value of roughly $2.63 trillion, within a 52 week range of about $196 to $279 (stockanalysis.com). Its trailing price to earnings ratio was about 29, which is far below its own ten year median of roughly 80, reflecting how much faster profit has grown than the share price. Analysts surveyed by S&P Global had an average twelve month forecast near $313, a figure we report as a third party data point rather than an endorsement; forecasts are opinions and frequently wrong.

The neutral way to frame the debate is to lay out what each side leans on. The constructive case rests on the re-acceleration of AWS, the high margin growth of advertising, the cost advantage of custom silicon, and the fact that the cash flow squeeze is caused by investment rather than by any decline in the underlying business. The cautious case rests on the same capital program compressing free cash flow, AWS slowly losing relative cloud share, the regulatory overhang, and the unproven return on hundreds of billions of dollars of AI spending. Nothing here is a prediction or a recommendation; it is a map of where the evidence points on each side.

Frequently asked questions

How does Amazon actually make most of its money?

By profit, most of it comes from Amazon Web Services, the cloud computing arm. In FY2025 AWS produced about 57 percent of Amazon's $80.0 billion in operating income while accounting for only about 18 percent of revenue. Retail generates the bulk of the $716.9 billion in sales but at thin margins, and a fast growing, high margin advertising business of $68.6 billion adds substantially to profit.

Why is Amazon designing its own chips?

To lower the cost of computing and reduce dependence on outside suppliers. Through its Annapurna Labs unit, Amazon designs the Nitro system that runs its servers, Graviton processors that replace many Intel and AMD chips, and Trainium and Inferentia chips for artificial intelligence. Amazon says Graviton now makes up more than half of the new processor capacity it adds, and its Trainium chips train large models, including for Anthropic, at a claimed cost advantage over standard GPUs. It has not replaced Nvidia, which still leads in frontier AI training.

What is the $200 billion that Amazon is spending on?

Capital expenditure, mostly data centers, AI chips, and the power and networking to run them, with smaller amounts for robotics and satellites. Chief executive Andy Jassy guided to about $200 billion of capital spending in 2026, up from $131.8 billion in 2025. The spending is the main reason Amazon's free cash flow fell from $38.2 billion to $11.2 billion over the past year.

Is Amazon still primarily a retailer?

By revenue, yes; by profit, no. The retail and marketplace businesses are most of the sales, but the cloud, advertising, and subscription businesses generate a disproportionate share of the earnings. That is why Amazon is better understood as several different companies sharing one logistics and technology backbone.

Sources

- Amazon.com FY2025 Form 10-K (annual report for the year ended December 31, 2025), U.S. Securities and Exchange Commission. https://www.sec.gov/Archives/edgar/data/1018724/000101872426000004/amzn-20251231.htm

- Amazon.com Q4 and full year 2025 earnings release. https://www.aboutamazon.com/news/company-news/amazon-earnings-q4-2025-report

- Amazon.com Q1 2026 earnings release and Form 10-Q. https://www.aboutamazon.com/news/company-news/amazon-earnings-q1-2026-report

- Synergy Research, cloud market share, Q1 2026. https://www.srgresearch.com/articles/cloud-market-annual-revenue-run-rate-topped-half-a-trillion-dollars-in-q1-as-growth-surge-continues

- AWS, Graviton5 and Trainium3 announcements, re:Invent 2025. https://www.aboutamazon.com/news/aws/aws-re-invent-2025-ai-news-updates

- Amazon, Project Rainier and the Anthropic investment. https://www.aboutamazon.com/news/aws/aws-project-rainier-ai-trainium-chips-compute-cluster

- Andy Jassy, 2025 letter to shareholders. https://www.aboutamazon.com/news/company-news/amazon-ceo-andy-jassy-2025-letter-to-shareholders

- Federal Trade Commission, FTC v. Amazon and the Prime settlement. https://www.ftc.gov/news-events/news/press-releases/2025/09/ftc-secures-historic-25-billion-settlement-against-amazon

- DataCenterDynamics, hyperscaler capital spending outlook. https://www.datacenterdynamics.com/en/news/us-hyperscaler-capex-to-top-700bn-in-2026-investors-fear-overbuild-and-weak-returns-moodys/

- stockanalysis.com, Amazon price, market value, and multiples. https://stockanalysis.com/stocks/amzn/

- · Kresmion compiled this study from Amazon's public filings and reputable reporting, as of June 21, 2026.

- · Amazon.com FY2025 Form 10-K, U.S. Securities and Exchange Commission. https://www.sec.gov/Archives/edgar/data/1018724/000101872426000004/amzn-20251231.htm

- · Amazon.com Q4 and full year 2025 earnings release. https://www.aboutamazon.com/news/company-news/amazon-earnings-q4-2025-report

- · Amazon.com Q1 2026 earnings release. https://www.aboutamazon.com/news/company-news/amazon-earnings-q1-2026-report

- · Synergy Research, cloud market share, Q1 2026. https://www.srgresearch.com/articles/cloud-market-annual-revenue-run-rate-topped-half-a-trillion-dollars-in-q1-as-growth-surge-continues

- · AWS, re:Invent 2025 (Graviton5, Trainium3). https://www.aboutamazon.com/news/aws/aws-re-invent-2025-ai-news-updates

- · Amazon, Project Rainier and the Anthropic investment. https://www.aboutamazon.com/news/aws/aws-project-rainier-ai-trainium-chips-compute-cluster

- · Andy Jassy, 2025 letter to shareholders. https://www.aboutamazon.com/news/company-news/amazon-ceo-andy-jassy-2025-letter-to-shareholders

- · Federal Trade Commission, FTC v. Amazon and the Prime settlement. https://www.ftc.gov/news-events/news/press-releases/2025/09/ftc-secures-historic-25-billion-settlement-against-amazon

- · DataCenterDynamics, hyperscaler capital spending outlook. https://www.datacenterdynamics.com/en/news/us-hyperscaler-capex-to-top-700bn-in-2026-investors-fear-overbuild-and-weak-returns-moodys/

- · stockanalysis.com, Amazon price, market value, and multiples. https://stockanalysis.com/stocks/amzn/

Kresmion publishes information, not investment advice. See our methodology and the latest research notes.

Kresmion is free during beta. A free account makes your watchlist permanent across devices and adds alerts when new signals fire. No card, about 30 seconds.

Start free