Study · Kresmion Research

The US Market Regime Right Now, in Numbers

As of June 15, 2026, Kresmion's cross-asset model reads the US market regime as Neutral with HIGH conviction (75%). In plain terms: the model sees no strong directional tilt either way, and its components mostly agree on that. This page walks through the numbers behind that read.

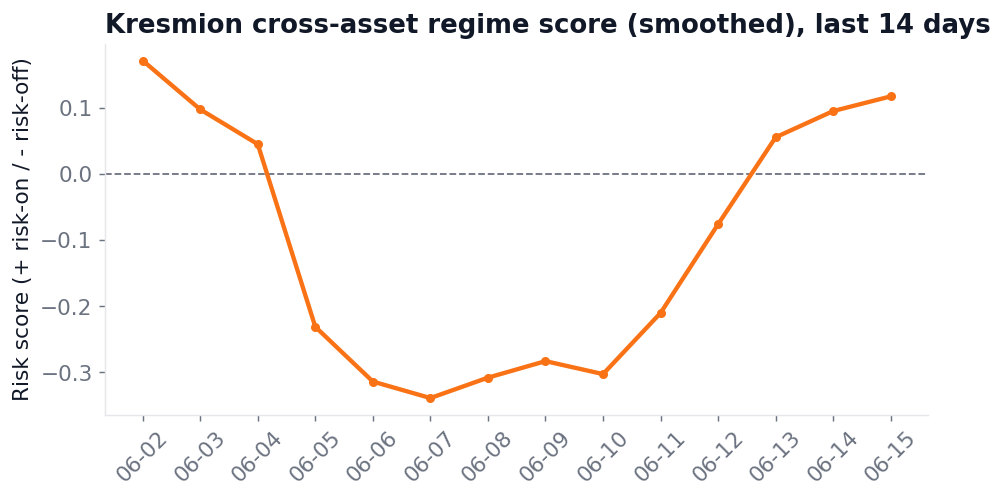

Kresmion rates the US market regime Neutral with HIGH conviction (75%), on a smoothed cross-asset risk score of +0.1179 that has just edged back above zero.

What the model says today

The Kresmion macro regime model fuses a basket of cross-asset and macro signals: equity trend and breadth, credit and high-yield spreads, rates and yield-curve shape, the dollar, VIX/MOVE volatility, commodities, and a net-liquidity aggregate built from the Fed balance sheet plus Treasury cash. Those inputs are z-scored against roughly one year of trailing history, weighted, exponentially smoothed, and mapped to five hysteresis buckets running from Strong Risk-Off to Strong Risk-On. The exact weights and bucket boundaries are not published. See the Kresmion methodology page for the full input list.

As of June 15, 2026, on that day's row of the Kresmion `macro_regime_history` dataset, the regime label is Neutral, the raw risk score is +0.1274, and the smoothed score is +0.1179. The model's conviction is HIGH at 75.00%, and the regime has held the Neutral label for 47 straight days. The latest row is not a transition day (`is_transition = false`), so the recent score swing happened *inside* the Neutral band rather than crossing into a new bucket.

The sign convention matters: positive readings tilt risk-on, negative readings tilt risk-off, and a smoothed value of +0.1179 sits close to neutral — consistent with the Neutral label. The 75% conviction figure is the model's stated confidence in the current classification, not a probability of forward returns.

Key takeaways

| Metric (Kresmion `macro_regime_history`, 2026-06-15) | Value |

|---|---|

| Regime label | Neutral |

| Smoothed risk score | +0.1179 |

| Raw risk score | +0.1274 |

| Conviction | HIGH (75.00%) |

| Regime age | 47 days |

| Largest positive factor | Volatility, +0.5824 |

The four factors, decomposed

The composite breaks into four factors on the June 15, 2026 row of the dataset:

| Factor | Reading | Role |

|---|---|---|

| Volatility | +0.5824 | Largest positive contributor |

| Growth | +0.4460 | Second-strongest |

| Liquidity | +0.0667 | Near flat |

| Risk appetite | -0.1559 | Only negative factor; a drag on the score |

The factor groupings are interpretive: Kresmion publishes the input list but not the exact input-to-factor mapping or the weights. With that caveat:

- Volatility captures the price-instability regime via VIX, MOVE, real-yield pressure, and breakeven compression. Inside it on June 15, 2026, the VIX z-score is -0.52, the MOVE z-score is -0.64, and the real-yield z-score is +0.53. A positive volatility factor here means a *calm, low-volatility* regime — so falling volatility reads as risk-supportive. The label can look counterintuitive: "high volatility factor" means "low actual volatility."

- Growth measures cyclical demand and economic momentum (PMI, economic surprise, the copper/gold ratio, jobless claims, and a yield-curve growth signal).

- Liquidity measures financial conditions and money availability via the net-liquidity aggregate, NFCI, real yields, and the dollar.

- Risk appetite measures willingness to hold risk through equity momentum (z = -0.58), high-yield spreads, AUD/JPY, and breakeven distance (z = -1.29).

What moved the score

The volatility factor drove the most recent change. Across June 10 to 15, 2026 it swung from -0.7488 to +0.5824 — a move of +1.33 — while the raw score moved from -0.3109 to +0.1274, a gain of +0.44.

The single largest day was June 11 to 12, 2026, when the volatility factor added +0.862 and the score added +0.152, while growth, liquidity, and risk appetite barely moved (d_growth +0.000, d_liquidity +0.148, d_risk_appetite +0.023). The model's own interpretation column confirms the read, describing the regime as "anchored chiefly by a strong volatility signal (+0.58) that outweighs the modest growth (+0.45) and liquidity (+0.07) factors."

The 14-day smoothed series traces a V-shape: it fell to a -0.3389 trough on June 7, 2026 and recovered above zero only in the final three days — +0.0560 on June 13, +0.0957 on June 14, and +0.1179 on June 15, 2026. Because the Neutral label has held for 47 days spanning both the dip and the current positive reading, the "neutral, high conviction" read is fresh and sits near a sign-flip boundary.

One caveat for reading day-to-day moves: some inputs update on a batch cadence, so daily factor changes can reflect data-refresh timing as well as fresh market action — the flat June 13-to-14 row and the step-function growth jump on June 9 are examples.

How it lines up with the wider picture

External developments corroborate the model's internal readings, though Kresmion does not ingest these specific articles.

- Fed meeting. Warsh's first FOMC meeting falls on June 16-17, 2026 and is an SEP and dot-plot meeting; markets price about a 97.4% chance of a hold at 3.50-3.75%, with attention on a possible shift away from an easing bias, per CoinGape.

- Inflation. Hot May 2026 inflation supports the elevated real-yield and compressed-breakeven readings inside the volatility factor: CPI ran +0.5% month over month and +4.2% year over year — a three-year high, per CNBC — while PPI rose +1.1% month over month against a +0.6% estimate and +6.5% year over year, the hottest since November 2022, per CBS News.

- Geopolitics. The US-Iran de-escalation reversed an oil and geopolitical-risk spike, with Brent down roughly 19% for May, aligning directionally with the volatility factor flipping positive as VIX and MOVE fell into mid-June, per CNBC.

Frequently asked questions

What is the US market regime as of June 15, 2026?

The Kresmion macro regime model labels it Neutral with HIGH conviction (75.00%), on a smoothed risk score of +0.1179 and a raw score of +0.1274, from the June 15, 2026 row of the `macro_regime_history` dataset.

Which factor is driving the regime score right now?

The volatility factor, at +0.5824 on June 15, 2026, is the largest positive contributor and accounts for most of the score's recovery from its June 7 trough. A positive volatility factor reflects a calm, low-volatility regime (VIX z = -0.52, MOVE z = -0.64).

Has the regime changed recently?

No. The Neutral label has held for 47 consecutive days, and June 15, 2026 is not a transition day. The smoothed score dipped to -0.3389 on June 7 and recovered above zero only in the last three days, so the swing occurred inside the Neutral band.

Does a high conviction reading predict returns?

No. The 75.00% conviction figure is the model's stated confidence in its current regime classification, not a probability of forward market returns.

---

Source: Kresmion Research, `macro_regime_history` dataset. This is information, not advice.

- · https://kresmion.com/about/methodology

- · https://coingape.com/fomc-meeting-what-to-expect-from-kevin-warsh-first-fed-decision-on-june-17/

- · https://www.cnbc.com/2026/06/10/cpi-inflation-report-may-2026.html

- · https://www.cbsnews.com/news/ppi-report-today-may-2026-highest-since-2022/

- · https://www.cnbc.com/2026/05/29/oil-prices-iran-ceasefire-us-trump-strait-hormuz-energy-costs.html

Kresmion publishes information, not investment advice. See our methodology and the latest research notes.

Kresmion is free during beta. A free account makes your watchlist permanent across devices and adds alerts when new signals fire. No card, about 30 seconds.

Start free